Article | Adaptive Spaces

Does the cost of living crisis mark the end of a rampant property market?

August 17, 2022 4 Minute Read

Residential property values have increased significantly over the last two years, with prices nearly 20% higher than they were at the start of 2020, according to ONS. Prices have been boosted by changes in household living and working patterns, stock shortages and government incentives have led to record house prices. Momentum continued into the start of 2022, as explored in more detail in our 2022 Market Outlook.

However, the tide may be beginning to turn as supply levels are beginning to catch up to demand and government incentives have ended. But, the proverbial straw that breaks the camel’s back could be the rising cost of living.

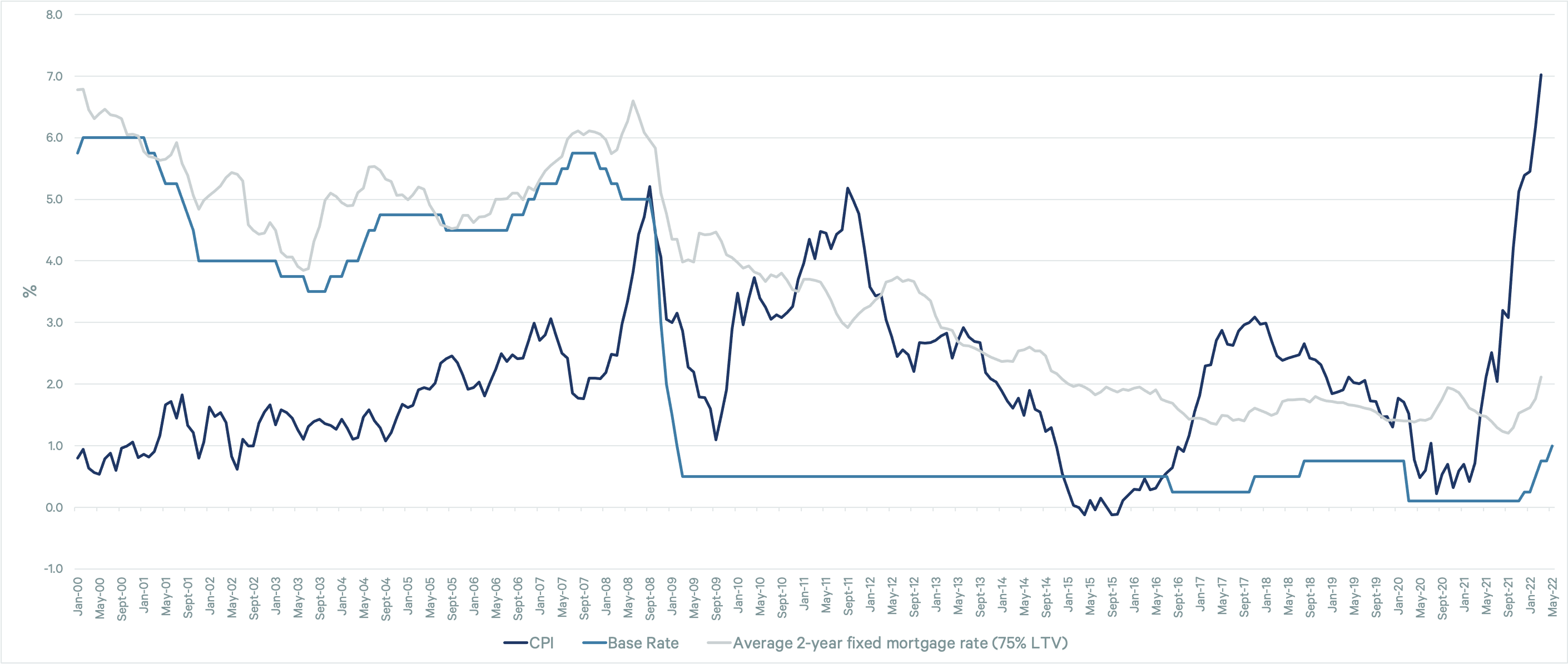

Inflation is at its highest level in 30 years. Being fuelled by hikes in energy bills and increasing fuel costs. We expect inflation to reach 7.0% by Q4 2022 The Bank of England is more pessimistic and forecasts inflation to peak at 10% in Q4.

As a result, the MPC increased the base rate to 1.0%. Its highest level since February 2009 - a time at which the economy was grappling with the fallout of the global financial crisis. At that point, the inflation rate was only 3.2% - less than half the current rate.

A rise in the base rate will in theory slow inflation by reducing consumer demand. But in the short term, it will compound the cost of living crisis by increasing mortgage costs. Those on variable or tracker rate mortgages will see an immediate hike in mortgage payments. Positively, however, the majority of mortgages, 74%, are on a fixed rate, according to UK finance, which will mitigate some of the affect, but it will make it harder and more expensive for new borrowers.

Figure 1: Inflation and interest rates

Source: ONS, Bank of England

In the six months to the end of March 2022, the average rate for a 2-year fixed mortgage at 75% LTV has increased by 91bp, from 1.2% to 2.11%. On a £300,000 property, this would add £97 to the monthly repayment costs, equal to £1,164 a year.

It isn’t just the actual cost of the mortgage, but the potential cost, which may weigh down on activity. As part of their affordability checks, banks carry out a borrower ‘stress test’. This assesses whether the buyer(s) could continue to afford the mortgage repayments should the interest rate increase to 3% above the lender’s Standard Variable Rate.

Given the recent and potential further rises in interest rates, the stress test could become a significant stumbling block for potential homebuyers. However, the Bank of England has begun a consultation on the removal of this test. Since household incomes have been squeezed, this could be a welcome change in helping households onto the housing ladder.

Overall though the combination of recent house price rises, the ongoing cost of living crisis, including rising interest rates, will slow the momentum in the housing market. But while we expect transaction levels to be lower in the second half of the year, overall they are likely to remain close to the long-term average.